Published on

Big Data and advanced analytics are critical topics for executives today. But many still aren't sure how to turn that promise into value. This presentation provides an overview of 16 examples and use ...

Big Data and advanced analytics are critical topics for executives today. But many still aren't sure how to turn that promise into value. This presentation provides an overview of 16 examples and use cases that lay out the different ways companies have approached the issue and found value: everything from pricing flexibility to customer preference management to credit risk analysis to fraud protection and discount targeting. For the latest on Big Data & Advanced Analytics: http://mckinseyonmarketingandsales.com/topics/big-data

- 1. Big Data and Advanced Analytics 16 Use Cases From a Practitioner's Perspective June 27th, 2013 Workshop at Nasscom Conference - by Invitation Any use of this material without specific permission of McKinsey & Company is strictly prohibited

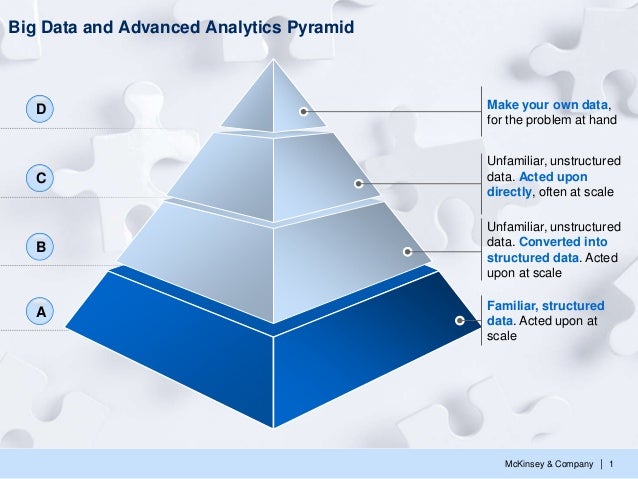

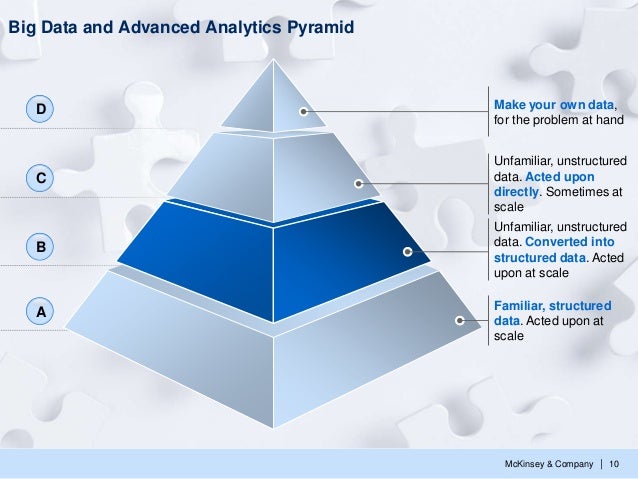

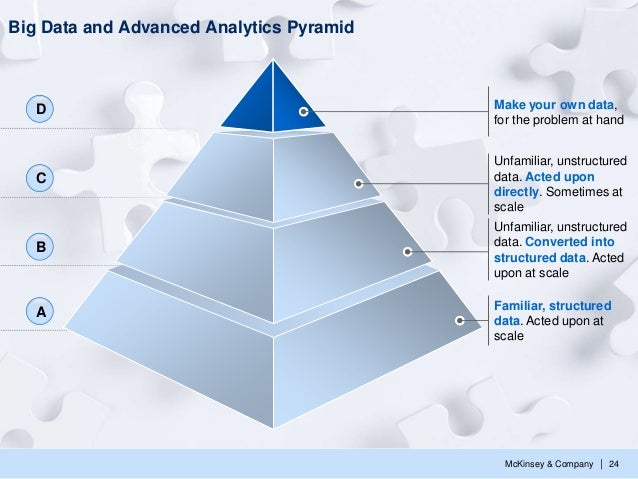

- 2. McKinsey & Company | 1 Big Data and Advanced Analytics Pyramid Make your own data, for the problem at hand Unfamiliar, unstructured data. Acted upon directly, often at scale Unfamiliar, unstructured data. Converted into structured data. Acted upon at scale Familiar, structured data. Acted upon at scale D C B A

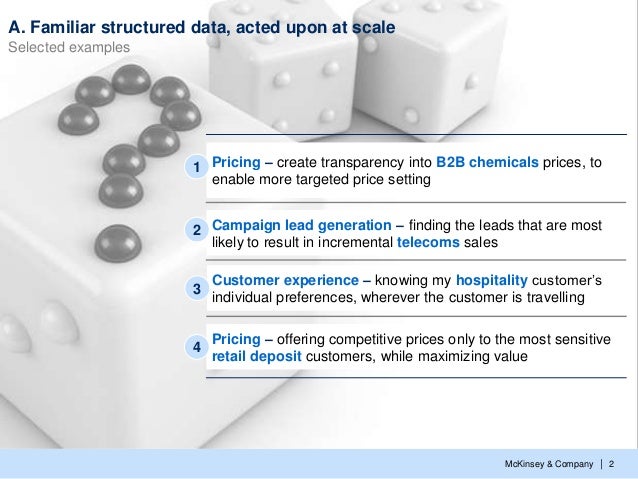

- 3. McKinsey & Company | 2 A. Familiar structured data, acted upon at scale Selected examples Campaign lead generation - finding the leads that are most likely to result in incremental telecoms sales 2 Pricing - offering competitive prices only to the most sensitive retail deposit customers, while maximizing value 4 Pricing - create transparency into B2B chemicals prices, to enable more targeted price setting 1 Customer experience - knowing my hospitality customer's individual preferences, wherever the customer is travelling 3

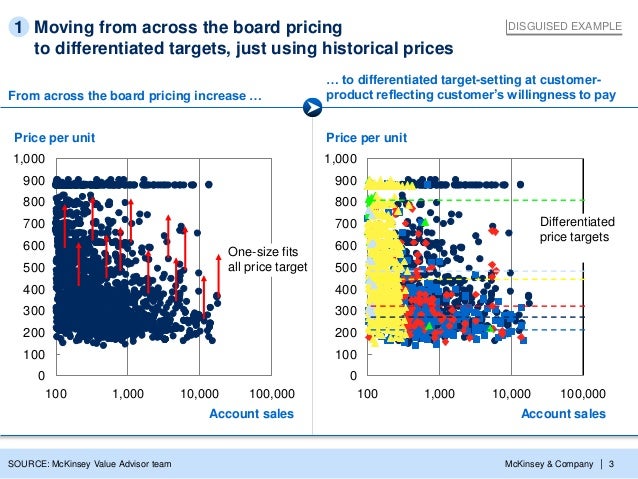

- 4. McKinsey & Company | 3 Moving from across the board pricing to differentiated targets, just using historical prices 0 100 200 300 400 500 600 700 800 900 1,000 Price per unit Account sales 100,00010,0001,000100 0 100 200 300 400 500 600 700 800 900 1,000 Account sales 100,00010,0001,000100 Price per unit Differentiated price targets One-size fits all price target DISGUISED EXAMPLE From across the board pricing increase ... ... to differentiated target-setting at customer- product reflecting customer's willingness to pay SOURCE: McKinsey Value Advisor team 1

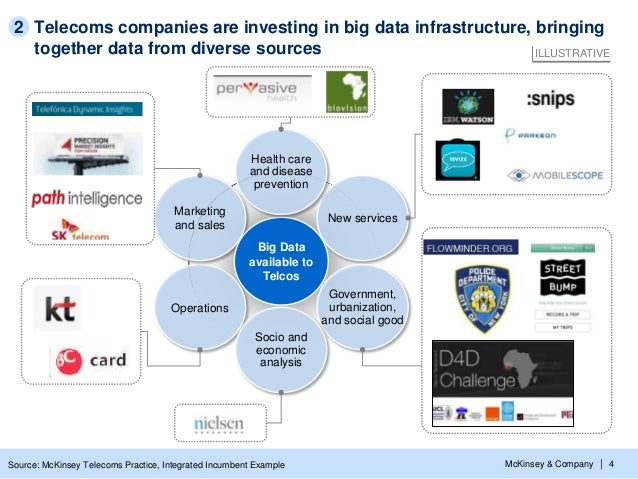

- 5. McKinsey & Company | 4 Telecoms companies are investing in big data infrastructure, bringing together data from diverse sources New services Government, urbanization, and social good Operations Marketing and sales Big Data available to Telcos Socio and economic analysis Health care and disease prevention ILLUSTRATIVE 2 Source: McKinsey Telecoms Practice, Integrated Incumbent Example

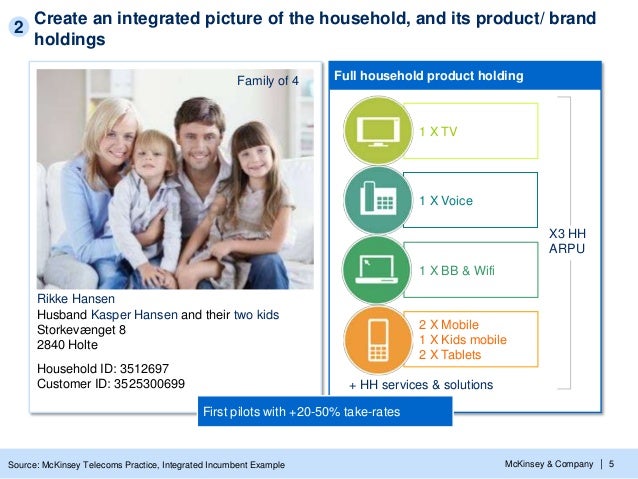

- 6. McKinsey & Company | 5 Create an integrated picture of the household, and its product/ brand holdings Full household product holdingFamily of 4 Rikke Hansen Husband Kasper Hansen and their two kids Storkevænget 8 2840 Holte Household ID: 3512697 Customer ID: 3525300699 1 X Voice 1 X BB & Wifi 2 X Mobile 1 X Kids mobile 2 X Tablets X3 HH ARPU 1 X TV + HH services & solutions First pilots with +20-50% take-rates Source: McKinsey Telecoms Practice, Integrated Incumbent Example 2

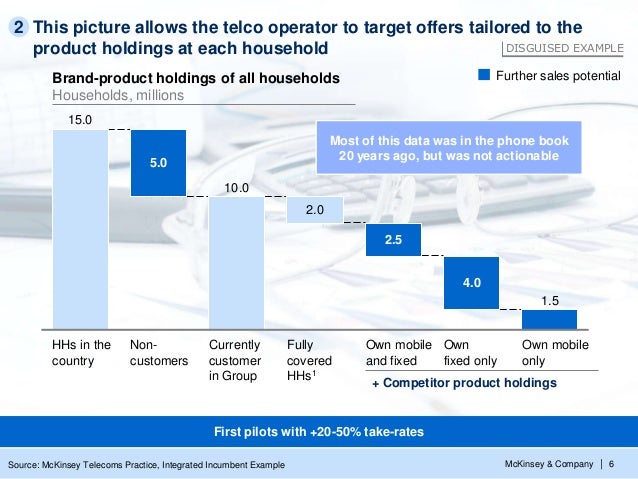

- 7. McKinsey & Company | 6 This picture allows the telco operator to target offers tailored to the product holdings at each household 15.0 HHs in the country 5.0 Non- customers 10.0 Currently customer in Group 2.0 Fully covered HHs1 2.5 Own mobile and fixed 4.0 Own fixed only 1.5 Own mobile only + Competitor product holdings Further sales potential DISGUISED EXAMPLE Most of this data was in the phone book 20 years ago, but was not actionable First pilots with +20-50% take-rates Source: McKinsey Telecoms Practice, Integrated Incumbent Example Brand-product holdings of all households Households, millions 2

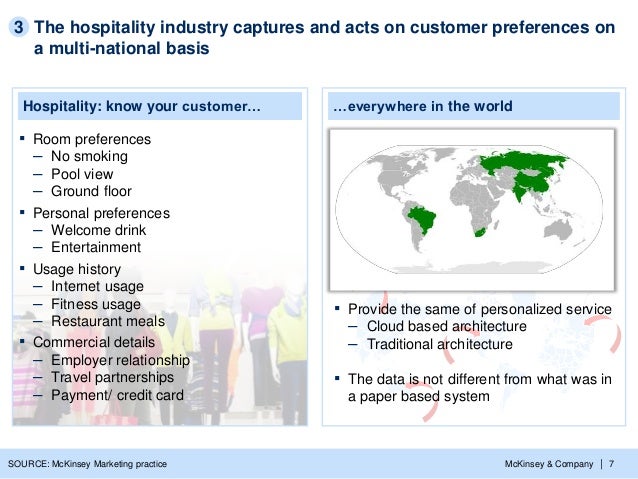

- 8. McKinsey & Company | 7 Hospitality: know your customer... ...everywhere in the world ▪ Commercial details - Employer relationship - Travel partnerships - Payment/ credit card ▪ Room preferences - No smoking - Pool view - Ground floor ▪ Personal preferences - Welcome drink - Entertainment ▪ Usage history - Internet usage - Fitness usage - Restaurant meals The hospitality industry captures and acts on customer preferences on a multi-national basis 3 ▪ Provide the same of personalized service - Cloud based architecture - Traditional architecture ▪ The data is not different from what was in a paper based system SOURCE: McKinsey Marketing practice

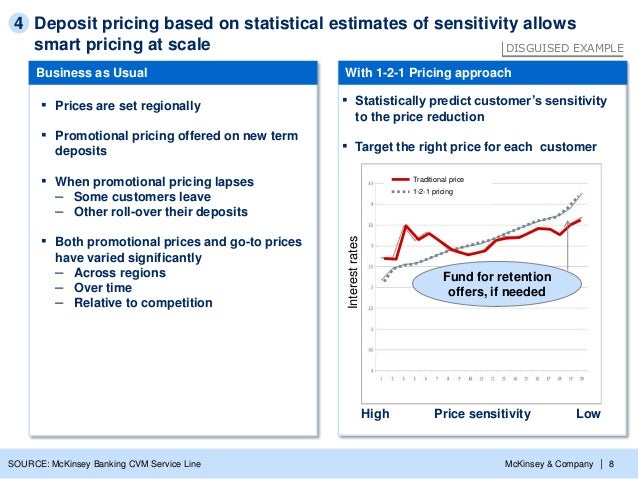

- 9. McKinsey & Company | 8 Deposit pricing based on statistical estimates of sensitivity allows smart pricing at scale 4 Business as Usual ▪ Prices are set regionally ▪ Promotional pricing offered on new term deposits ▪ When promotional pricing lapses - Some customers leave - Other roll-over their deposits ▪ Both promotional prices and go-to prices have varied significantly - Across regions - Over time - Relative to competition With 1-2-1 Pricing approach ▪ Statistically predict customer's sensitivity to the price reduction ▪ Target the right price for each customer LowHigh Price sensitivity Fund for retention offers, if needed Interestrates 1-2-1 pricing Traditional price DISGUISED EXAMPLE SOURCE: McKinsey Banking CVM Service Line

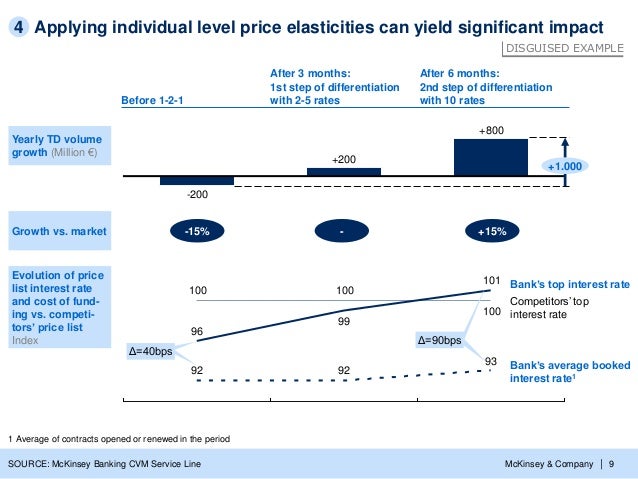

- 10. McKinsey & Company | 9 Applying individual level price elasticities can yield significant impact -200 +800 +1.000 +200 Evolution of price list interest rate and cost of fund- ing vs. competi- tors' price list Index Yearly TD volume growth (Million €) After 3 months: 1st step of differentiation with 2-5 ratesBefore 1-2-1 100 100100 101 99 96 93 9292 Competitors' top interest rate Bank's top interest rate Bank's average booked interest rate1 Growth vs. market After 6 months: 2nd step of differentiation with 10 rates -15% - +15% Δ=40bps Δ=90bps 1 Average of contracts opened or renewed in the period SOURCE: McKinsey Banking CVM Service Line 4 DISGUISED EXAMPLE

- 11. McKinsey & Company | 10 Big Data and Advanced Analytics Pyramid Make your own data, for the problem at hand Unfamiliar, unstructured data. Acted upon directly. Sometimes at scale Unfamiliar, unstructured data. Converted into structured data. Acted upon at scale Familiar, structured data. Acted upon at scale D C B A

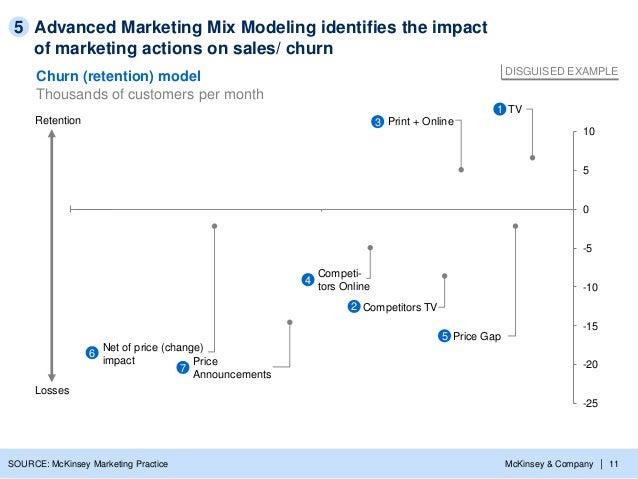

- 12. McKinsey & Company | 11 -25 -20 -15 -10 -5 0 5 10 Print + Online Net of price (change) impact Competi- tors Online Competitors TV Price Announcements Price Gap Retention Losses Advanced Marketing Mix Modeling identifies the impact of marketing actions on sales/ churn Churn (retention) model Thousands of customers per month TV 4 5 3 2 6 7 1 DISGUISED EXAMPLE 5 SOURCE: McKinsey Marketing Practice

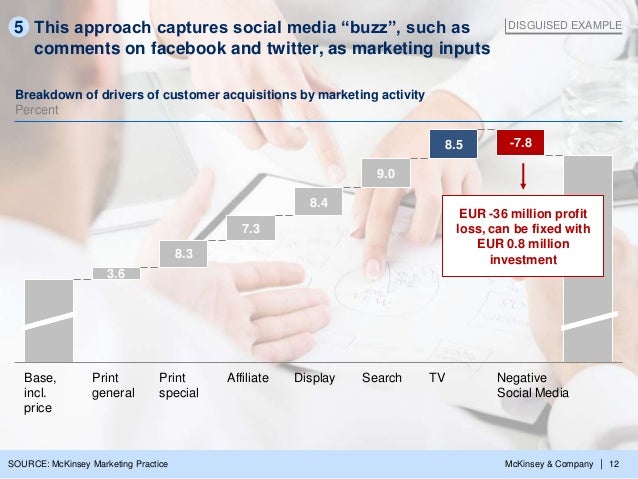

- 13. McKinsey & Company | 12 This approach captures social media "buzz", such as comments on facebook and twitter, as marketing inputs Breakdown of drivers of customer acquisitions by marketing activity Percent Print special Print general Base, incl. price Negative Social Media TVSearchDisplayAffiliate 7.3 8.3 3.6 -7.88.5 9.0 8.4 EUR -36 million profit loss, can be fixed with EUR 0.8 million investment 5 DISGUISED EXAMPLE SOURCE: McKinsey Marketing Practice

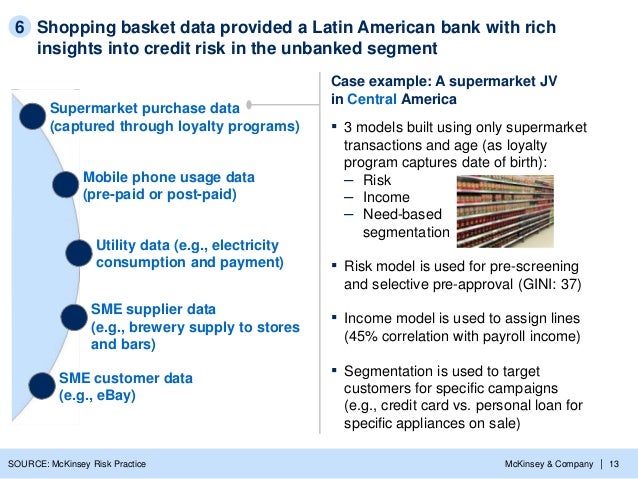

- 14. McKinsey & Company | 13 Supermarket purchase data (captured through loyalty programs) Mobile phone usage data (pre-paid or post-paid) SME supplier data (e.g., brewery supply to stores and bars) SME customer data (e.g., eBay) Utility data (e.g., electricity consumption and payment) Case example: A supermarket JV in Central America ▪ 3 models built using only supermarket transactions and age (as loyalty program captures date of birth): - Risk - Income - Need-based segmentation ▪ Risk model is used for pre-screening and selective pre-approval (GINI: 37) ▪ Income model is used to assign lines (45% correlation with payroll income) ▪ Segmentation is used to target customers for specific campaigns (e.g., credit card vs. personal loan for specific appliances on sale) Shopping basket data provided a Latin American bank with rich insights into credit risk in the unbanked segment 6 SOURCE: McKinsey Risk Practice

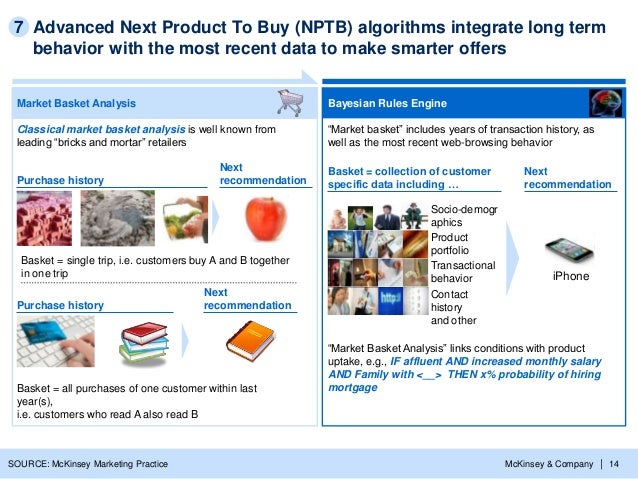

- 15. McKinsey & Company | 14 Advanced Next Product To Buy (NPTB) algorithms integrate long term behavior with the most recent data to make smarter offers 7 Market Basket Analysis Bayesian Rules Engine Classical market basket analysis is well known from leading "bricks and mortar" retailers "Market Basket Analysis" links conditions with product uptake, e.g., IF affluent AND increased monthly salary AND Family with <__> THEN x% probability of hiring mortgage Basket = single trip, i.e. customers buy A and B together in one trip Basket = all purchases of one customer within last year(s), i.e. customers who read A also read B "Market basket" includes years of transaction history, as well as the most recent web-browsing behavior Next recommendationPurchase history Next recommendationPurchase history Next recommendation Product portfolio Transactional behavior Contact history and other Socio-demogr aphics Basket = collection of customer specific data including ... iPhone SOURCE: McKinsey Marketing Practice

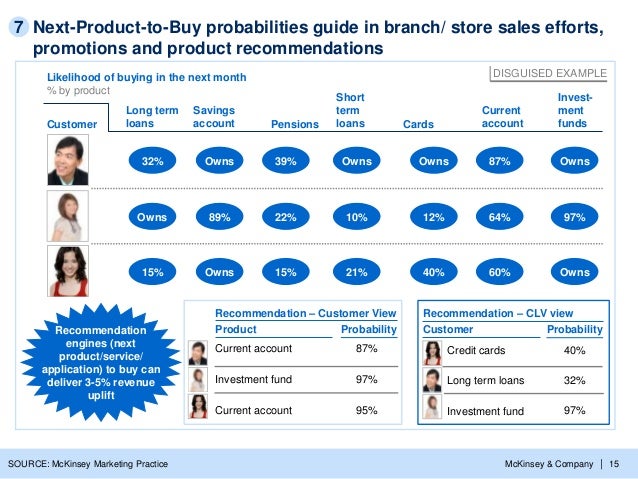

- 16. McKinsey & Company | 15 Next-Product-to-Buy probabilities guide in branch/ store sales efforts, promotions and product recommendations SOURCE: McKinsey Marketing Practice Customer Likelihood of buying in the next month % by product Long term loans 32% Owns 15% Savings account Owns 89% Owns Pensions 39% 22% 15% Short term loans Owns 10% 21% Cards Owns 12% 40% Current account 87% 64% 60% Invest- ment funds Owns 97% Owns Product Probability 87% Investment fund 97% Current account 95% Recommendation - Customer View Current account Customer Probability 40% 32% 97% Recommendation - CLV view Recommendation engines (next product/service/ application) to buy can deliver 3-5% revenue uplift Long term loans Investment fund Credit cards 7 DISGUISED EXAMPLE

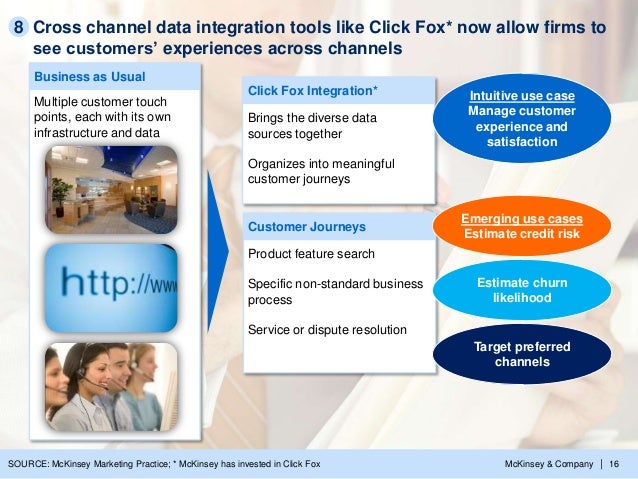

- 17. McKinsey & Company | 16 Cross channel data integration tools like Click Fox* now allow firms to see customers' experiences across channels Business as Usual Multiple customer touch points, each with its own infrastructure and data Click Fox Integration* Brings the diverse data sources together Organizes into meaningful customer journeys Customer Journeys Product feature search Specific non-standard business process Service or dispute resolution Intuitive use case Manage customer experience and satisfaction Emerging use cases Estimate credit risk Estimate churn likelihood Target preferred channels 8 SOURCE: McKinsey Marketing Practice; * McKinsey has invested in Click Fox

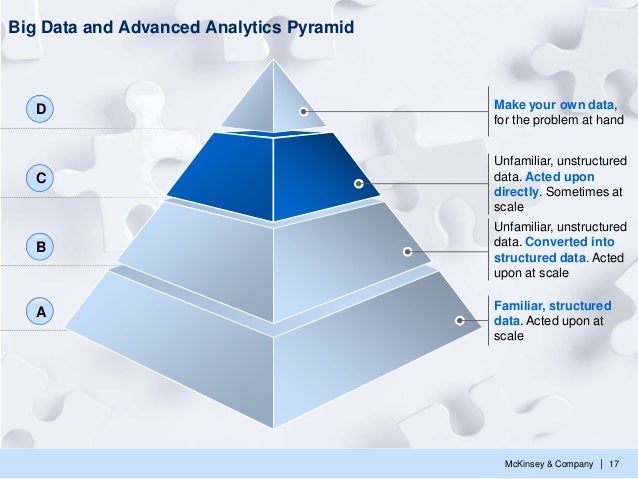

- 18. McKinsey & Company | 17 Big Data and Advanced Analytics Pyramid Make your own data, for the problem at hand Unfamiliar, unstructured data. Acted upon directly. Sometimes at scale Unfamiliar, unstructured data. Converted into structured data. Acted upon at scale Familiar, structured data. Acted upon at scale D C B A

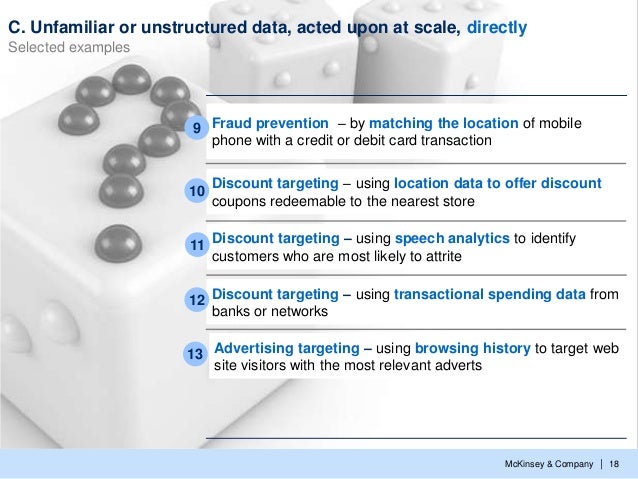

- 19. McKinsey & Company | 18 C. Unfamiliar or unstructured data, acted upon at scale, directly Selected examples Discount targeting - using location data to offer discount coupons redeemable to the nearest store 10 Discount targeting - using transactional spending data from banks or networks 12 Fraud prevention - by matching the location of mobile phone with a credit or debit card transaction 9 Discount targeting - using speech analytics to identify customers who are most likely to attrite 11 13 Advertising targeting - using browsing history to target web site visitors with the most relevant adverts

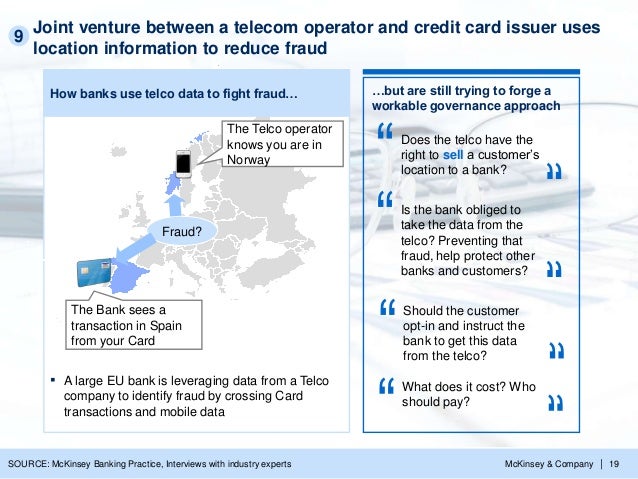

- 20. McKinsey & Company | 19 Joint venture between a telecom operator and credit card issuer uses location information to reduce fraud How banks use telco data to fight fraud... ▪ A large EU bank is leveraging data from a Telco company to identify fraud by crossing Card transactions and mobile data The Bank sees a transaction in Spain from your Card The Telco operator knows you are in Norway Fraud? 9 ...but are still trying to forge a workable governance approach Does the telco have the right to sell a customer's location to a bank? Is the bank obliged to take the data from the telco? Preventing that fraud, help protect other banks and customers? Should the customer opt-in and instruct the bank to get this data from the telco? What does it cost? Who should pay? SOURCE: McKinsey Banking Practice, Interviews with industry experts

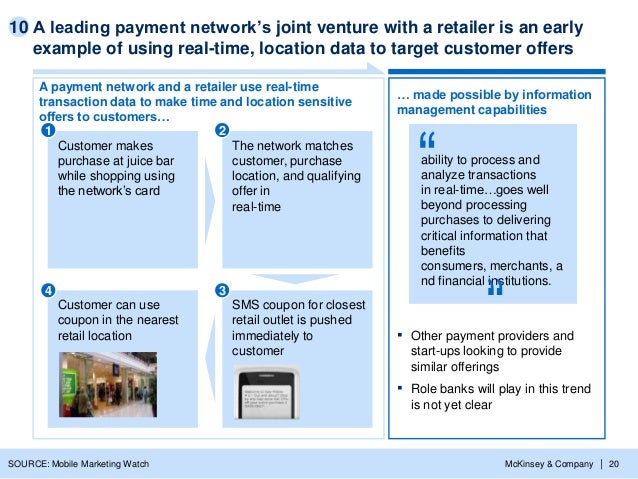

- 21. McKinsey & Company | 20 A leading payment network's joint venture with a retailer is an early example of using real-time, location data to target customer offers SOURCE: Mobile Marketing Watch A payment network and a retailer use real-time transaction data to make time and location sensitive offers to customers... ... made possible by information management capabilities ability to process and analyze transactions in real-time...goes well beyond processing purchases to delivering critical information that benefits consumers, merchants, a nd financial institutions. ▪ Other payment providers and start-ups looking to provide similar offerings ▪ Role banks will play in this trend is not yet clear SMS coupon for closest retail outlet is pushed immediately to customer Customer makes purchase at juice bar while shopping using the network's card Customer can use coupon in the nearest retail location The network matches customer, purchase location, and qualifying offer in real-time 1 2 4 3 10

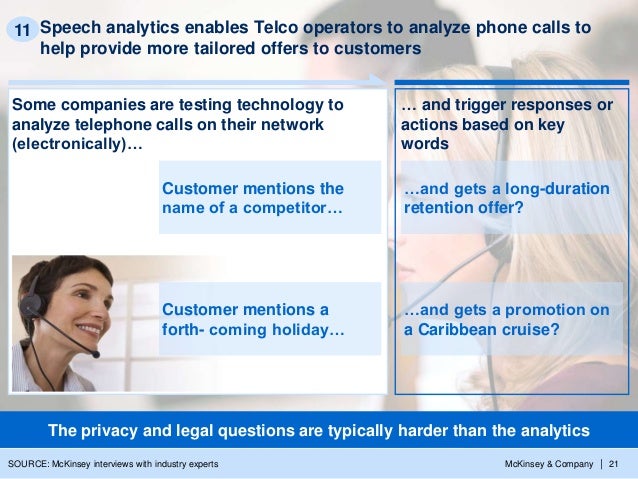

- 22. McKinsey & Company | 21 Speech analytics enables Telco operators to analyze phone calls to help provide more tailored offers to customers 11 The privacy and legal questions are typically harder than the analytics Some companies are testing technology to analyze telephone calls on their network (electronically)... ... and trigger responses or actions based on key words ...and gets a long-duration retention offer? ...and gets a promotion on a Caribbean cruise? Customer mentions the name of a competitor... Customer mentions a forth- coming holiday... SOURCE: McKinsey interviews with industry experts

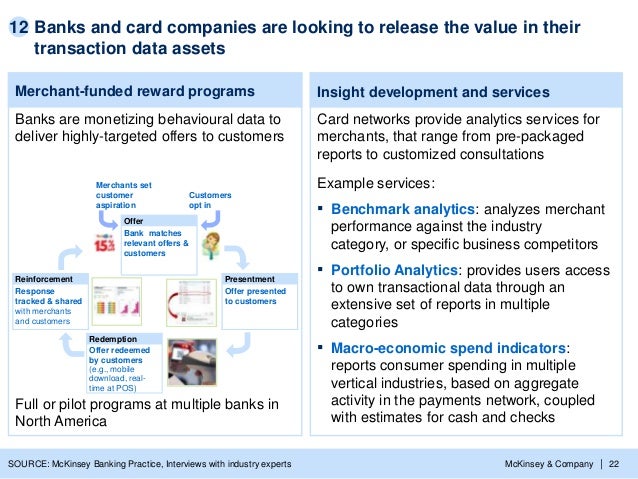

- 23. McKinsey & Company | 22 Banks and card companies are looking to release the value in their transaction data assets Merchant-funded reward programs Banks are monetizing behavioural data to deliver highly-targeted offers to customers Insight development and services Card networks provide analytics services for merchants, that range from pre-packaged reports to customized consultations Customers opt in Offer Bank matches relevant offers & customers Offer Bank matches relevant offers & customers Reinforcement Response tracked & shared with merchants and customers Reinforcement Response tracked & shared with merchants and customers Redemption Offer redeemed by customers (e.g., mobile download, real- time at POS) Merchants set customer aspiration Presentment Offer presented to customers Presentment Offer presented to customers Full or pilot programs at multiple banks in North America Example services: ▪ Benchmark analytics: analyzes merchant performance against the industry category, or specific business competitors ▪ Portfolio Analytics: provides users access to own transactional data through an extensive set of reports in multiple categories ▪ Macro-economic spend indicators: reports consumer spending in multiple vertical industries, based on aggregate activity in the payments network, coupled with estimates for cash and checks 12 SOURCE: McKinsey Banking Practice, Interviews with industry experts

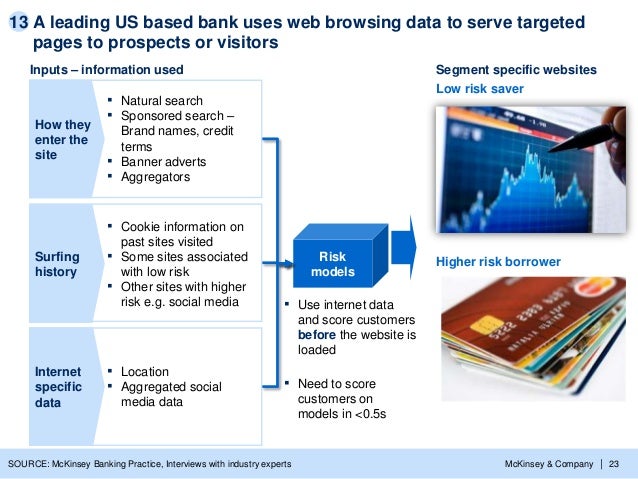

- 24. McKinsey & Company | 23 A leading US based bank uses web browsing data to serve targeted pages to prospects or visitors Risk models Segment specific websitesInputs - information used How they enter the site Internet specific data Surfing history ▪ Use internet data and score customers before the website is loaded ▪ Need to score customers on models in <0.5s Low risk saver Higher risk borrower ▪ Location ▪ Aggregated social media data ▪ Cookie information on past sites visited ▪ Some sites associated with low risk ▪ Other sites with higher risk e.g. social media ▪ Natural search ▪ Sponsored search - Brand names, credit terms ▪ Banner adverts ▪ Aggregators 13 SOURCE: McKinsey Banking Practice, Interviews with industry experts

- 25. McKinsey & Company | 24 Big Data and Advanced Analytics Pyramid Make your own data, for the problem at hand Unfamiliar, unstructured data. Acted upon directly. Sometimes at scale Unfamiliar, unstructured data. Converted into structured data. Acted upon at scale Familiar, structured data. Acted upon at scale D C B A

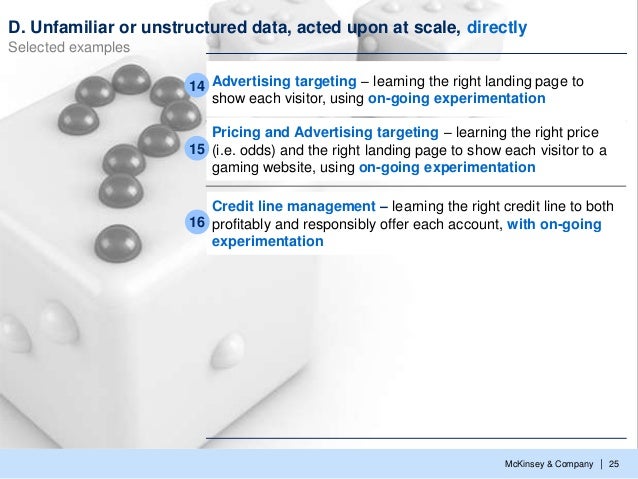

- 26. McKinsey & Company | 25 D. Unfamiliar or unstructured data, acted upon at scale, directly Selected examples Pricing and Advertising targeting - learning the right price (i.e. odds) and the right landing page to show each visitor to a gaming website, using on-going experimentation 15 Advertising targeting - learning the right landing page to show each visitor, using on-going experimentation 14 Credit line management - learning the right credit line to both profitably and responsibly offer each account, with on-going experimentation 16

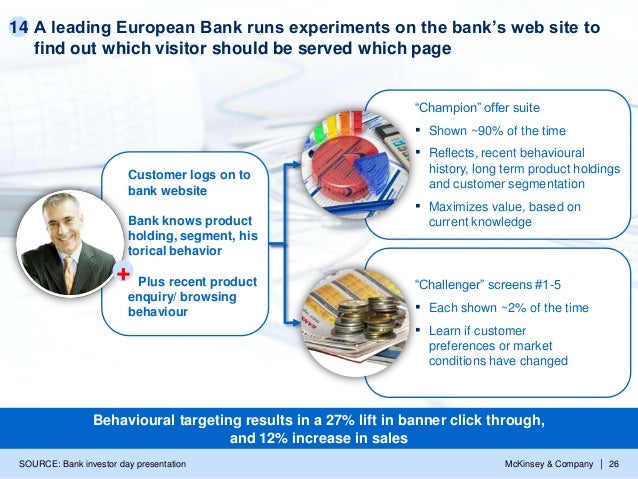

- 27. McKinsey & Company | 26 A leading European Bank runs experiments on the bank's web site to find out which visitor should be served which page 14 Customer logs on to bank website Bank knows product holding, segment, his torical behavior Plus recent product enquiry/ browsing behaviour "Champion" offer suite ▪ Shown ~90% of the time ▪ Reflects, recent behavioural history, long term product holdings and customer segmentation ▪ Maximizes value, based on current knowledge "Challenger" screens #1-5 ▪ Each shown ~2% of the time ▪ Learn if customer preferences or market conditions have changed SOURCE: Bank investor day presentation + Behavioural targeting results in a 27% lift in banner click through, and 12% increase in sales

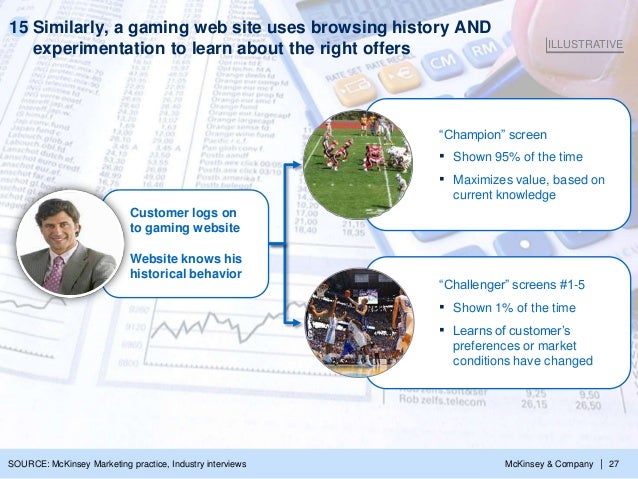

- 28. McKinsey & Company | 27 Similarly, a gaming web site uses browsing history AND experimentation to learn about the right offers 15 ILLUSTRATIVE Customer logs on to gaming website Website knows his historical behavior "Champion" screen ▪ Shown 95% of the time ▪ Maximizes value, based on current knowledge "Challenger" screens #1-5 ▪ Shown 1% of the time ▪ Learns of customer's preferences or market conditions have changed SOURCE: McKinsey Marketing practice, Industry interviews

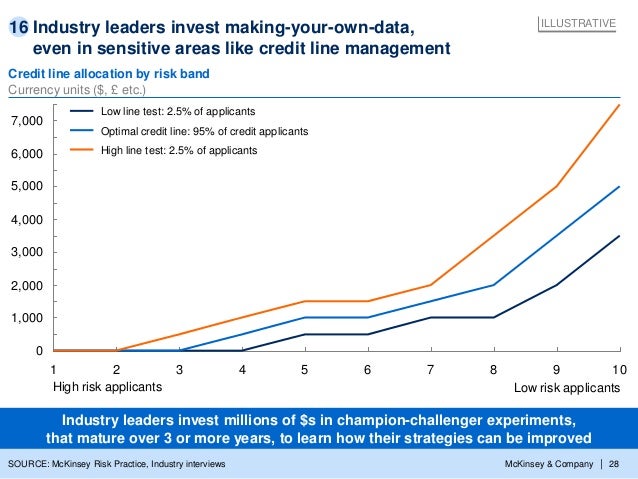

- 29. McKinsey & Company | 28 Industry leaders invest making-your-own-data, even in sensitive areas like credit line management SOURCE: McKinsey Risk Practice, Industry interviews 1 2 3 4 5 6 7 8 9 10 0 1,000 2,000 3,000 4,000 5,000 6,000 7,000 Low line test: 2.5% of applicants Optimal credit line: 95% of credit applicants High line test: 2.5% of applicants ILLUSTRATIVE Credit line allocation by risk band Currency units ($, £ etc.) Low risk applicantsHigh risk applicants Industry leaders invest millions of $s in champion-challenger experiments, that mature over 3 or more years, to learn how their strategies can be improved 16

- 30. McKinsey & Company | 29 Education BA from St. Stephen's College, Delhi MBA from University of Chicago, Graduate School of Business Work experience McKinsey experience includes: Consumer banking B2B marketing Functional focus Advanced Analytics, Customer Lifecycle Management, Credit Risk Sectors Financial Services, Consumer Products Prithvi Chandrasekhar Senior Expert, Marketing, London Office @McK_CMSOForum www.youtube.com/McKinseyCMSOforumwww.cmsoforum.mckinsey.comWWW http://www.slideshare.net/McK_CMSOForum Stay Connected:

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

How to get the most from big data Page 3 Page 5

How to get the most from big data Page 3 Page 5